Ondo Finance said Ripple has redeemed OUSG on XRP Ledger and received a USD payout in Singapore through Mastercard and Kinexys by J.P. Morgan.

The May 6 pilot tested whether a tokenized fund redemption on a public blockchain could trigger a bank-account payout across borders and banks, using a transaction path that Ondo said operated outside traditional banking windows.

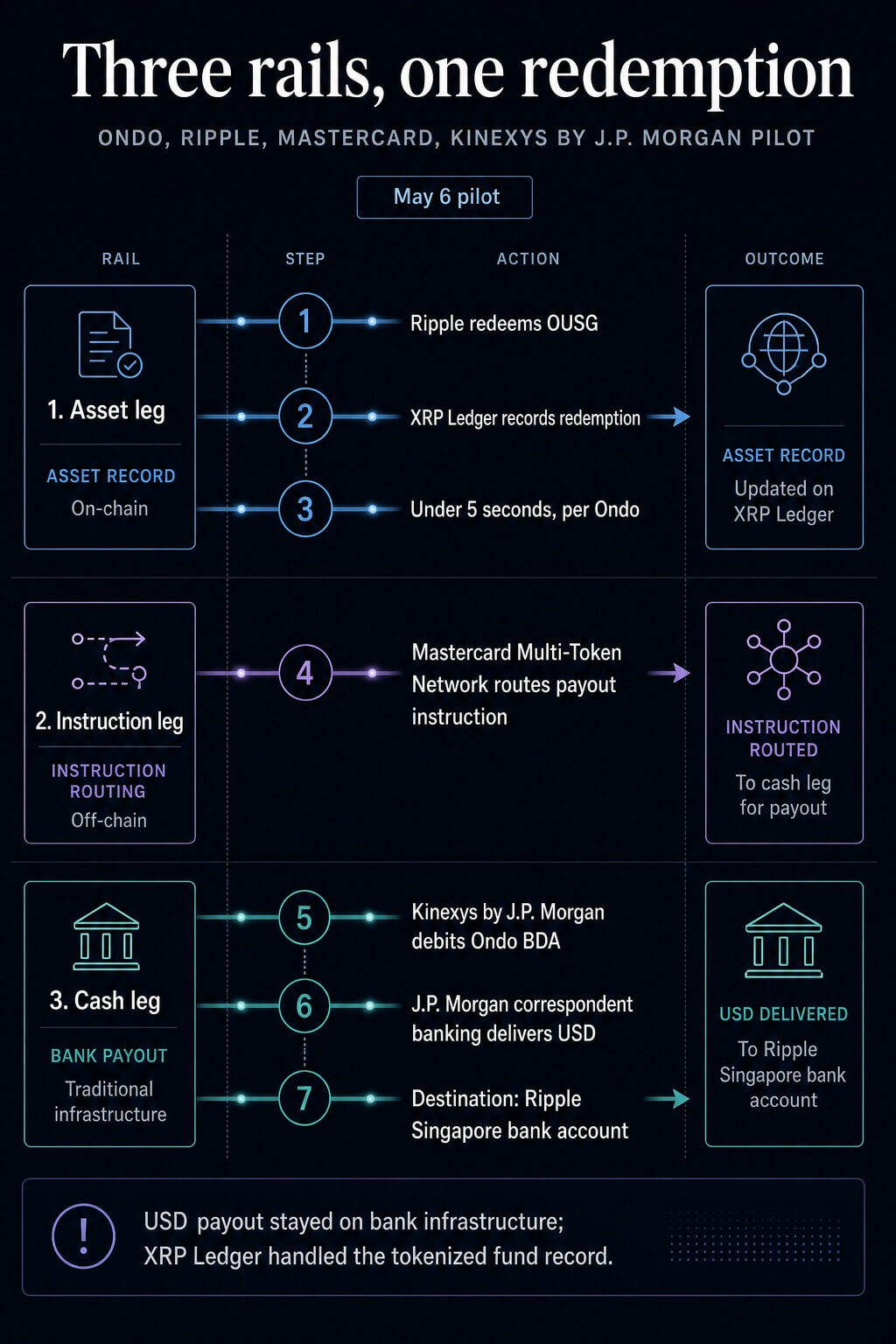

Ondo said the XRP Ledger leg processed in under five seconds. The cash leg stayed inside bank infrastructure, moving through Mastercard’s Multi-Token Network, Kinexys by J.P. Morgan, and J.P. Morgan’s correspondent banking network.

That split is the core of the development. The pilot links public-chain settlement speed to bank-account completion while keeping the USD payout on bank infrastructure. The available record separates XRP Ledger’s asset role from the USD payout, which was initiated on Kinexys and delivered to Ripple’s Singapore bank account through J.P. Morgan’s rails.

How the settlement chain was divided

Ondo described the transaction as the first near-real-time, cross-border, cross-bank redemption of a tokenized U.S. Treasury fund. Ripple redeemed part of its Ondo Short-Term U.S. Government Treasuries holdings on XRP Ledger.

The redemption then moved into a payout path. Ondo processed the request, Mastercard’s Multi-Token Network routed the instruction, Kinexys debited Ondo’s Blockchain Deposit Account, and J.P. Morgan’s correspondent banking network delivered the USD proceeds to Ripple’s Singapore bank account.

| Leg | Actor or rail | What it did | Practical effect |

|---|---|---|---|

| Asset leg | XRP Ledger | Recorded the OUSG redemption | Ondo said this leg processed in under five seconds |

| Instruction leg | Mastercard Multi-Token Network | Routed the fiat payout instruction | Connected the onchain redemption to bank settlement infrastructure |

| Cash leg | Kinexys by J.P. Morgan and J.P. Morgan correspondent banking | Moved USD proceeds to Ripple’s Singapore bank account | Kept fiat completion inside regulated bank rails |

The structure shows how the asset record, instruction layer, and fiat payout can be coordinated so an institution can avoid a separate manual process after a tokenized fund redemption.

XRP Ledger documentation says new ledger versions usually close about every three to five seconds, which supports the plausibility of a fast asset leg. The pilot-specific processing time and first-of-its-kind framing remain attributed to Ondo.

Ondo’s June 2025 launch brought the tokenized Treasury product to XRPL with minting and redemption support tied to Ripple’s RLUSD stablecoin, and CryptoSlate covered that launch at the time.

The fresh peg is the redemption-to-bank-account path. Ripple’s OUSG redemption was tied to a cross-border payout route involving Mastercard and J.P. Morgan infrastructure, building on the tokenized fund’s existing XRPL deployment.

Kinexys also entered the pilot with prior tokenized-settlement work behind it. J.P. Morgan’s blockchain unit had already completed a tokenized Treasury settlement test with Ondo and Chainlink in 2025, using a delivery-versus-payment structure that connected Kinexys Digital Payments to Ondo Chain testnet activity.

CryptoSlate covered that Kinexys-Ondo test as an earlier bridge between bank payment rails and tokenized asset markets. The May 2026 pilot extends that baseline into a different pattern: OUSG redemption on the XRP Ledger, a payout instruction via Mastercard, and a USD payment to a Singapore bank account.

Mastercard’s role also fits a prior setup. The company announced Ondo in 2025 as the first tokenized real-world asset provider on its Multi-Token Network, describing MTN as a way to link commercial banks with digital assets that can move around the clock. In this pilot, MTN served as the routing layer between on-chain redemption and Kinexys settlement, with the issuer and dollar-settlement roles handled elsewhere.

Scale gives the pilot useful context

OUSG is a qualified-access product. Ondo’s documentation describes it as tokenized exposure primarily to short-term U.S. Treasuries and government-sponsored enterprise securities, with access limited to eligible investors who complete onboarding for Ondo’s qualified-access products.

That restriction changes the likely near-term audience. The first users of this type of settlement design are more likely to be funds, payment firms, market makers, treasury teams, or financial institutions managing tokenized collateral and cash positions across time zones.

The setup points first toward institutional settlement design, with consumer-facing access left to other product channels.

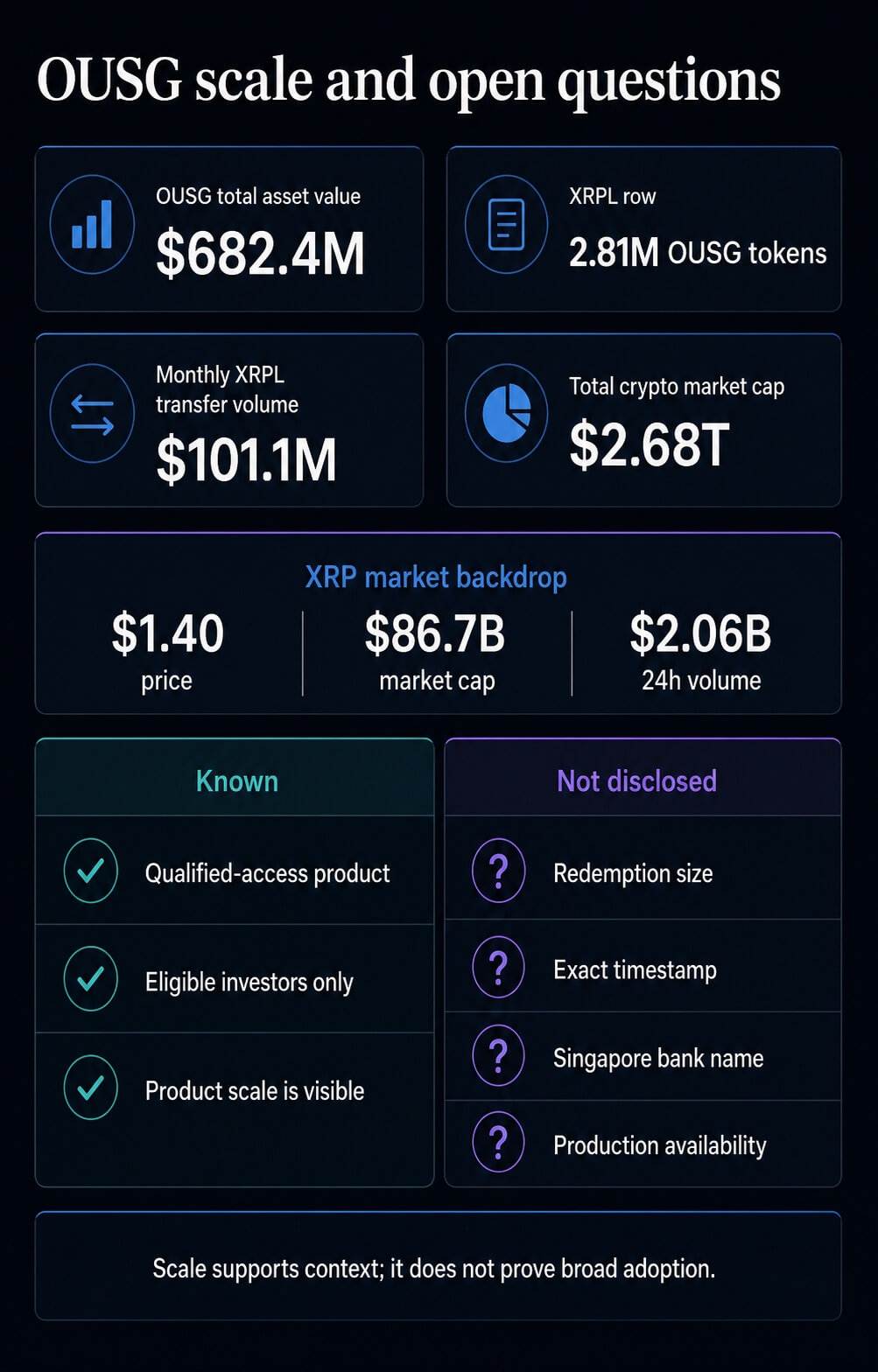

RWA.xyz showed OUSG with a total asset value of about $680 million when accessed on May 9. The same page showed XRP Ledger as one of the product’s supported networks, with roughly 2.8 million OUSG tokens on XRPL and about $101 million in monthly transfer volume associated with the XRPL row. Ethereum, meanwhile, holds around $2.4 million in tokens.

Those figures give the product scale while leaving the pilot itself unquantified. Ondo’s release did not disclose how much OUSG Ripple redeemed, the exact timestamp of the transaction, the Singapore bank involved, or whether the process is now available beyond the pilot participants.

The product data also shows why the transaction should be treated as infrastructure context before adoption proof. OUSG is large enough to be a relevant tokenized Treasury instrument, and the XRPL row points to activity around the product.

The same data leaves this specific redemption undisclosed, so the scale belongs in the background rather than in the lede claim.

For XRP, the market backdrop is separate from the settlement claim. CryptoSlate’s XRP page listed the token at around $1.42, with roughly $86 billion in market cap and about $2 billion in 24-hour volume.

CryptoSlate’s aggregate market page listed the total crypto market cap at about $2.68 trillion.

Repeatability is the next test

The pilot lands inside a larger tokenization debate. Ripple and Boston Consulting Group projected in 2025 that tokenized real-world assets could grow to $18.9 trillion by 2033.

That figure is useful as a scenario marker, but it comes from a Ripple release about a Ripple-BCG report and should be treated as participant forecast context.

The operational test is more concrete than the forecast. Tokenized Treasuries already make sense on paper as collateral, cash-management instruments, and yield-bearing assets that can move on ledgers outside market hours.

The harder question is whether redemptions can settle into bank accounts while reducing the batch processes, cutoffs, and manual instructions that tokenization is supposed to shrink.

Ondo, Ripple, Mastercard, and Kinexys have now shown one controlled answer: public-chain redemption records can be coordinated with interbank settlement infrastructure. That is a real infrastructure step, but it remains a pilot with missing details.

The signal to watch is whether the same structure becomes available to more institutions, larger transaction sizes, more banks, or more public blockchains where OUSG is issued.

If it does, tokenized Treasury products become less like blockchain wrappers around familiar assets and more like operating components in cross-border liquidity management. A bespoke transaction among named partners would keep the development closer to infrastructure validation than market transformation.

For now, the important detail is the split. XRP Ledger handled the tokenized fund record quickly. Mastercard and Kinexys connected that event to bank instructions. J.P. Morgan’s network delivered USD.

The pilot’s strongest message is that tokenized funds may be moving toward a model where public ledgers and bank rails have to work together in the same transaction.